At the start of the year, we cautioned that after three strong years in the stock markets, investors need to have realistic expectations about near-term returns and be prepared for a period of possible market declines.

The exact timing and reason for the decline were always going to be impossible to predict, but we now know that the United States and Israel’s strikes on Iran were the catalyst for this year’s uncertainty.

The disruption to global oil supply, coupled with ongoing uncertainty about the extent of AI’s impact on the labour market, has led the market to seek answers that don’t yet exist.

At the time of writing, many global markets are sitting at, or very near, “correction” levels. This is a technical term meaning it is down 10% from its most recent high-water mark.

Not one concern, but many

As we see it, the market is demanding certainty about three distinct risk factors.

What can we expect from the US-Iran conflict?

Particularly unsettling about the current conflict is the confusion about the US government’s aims and whether this level of action was warranted. While geopolitical conflicts always introduce uncertainty, the anxiety is heightened when the US president can change the sentiment with a single social media post.

If the conflict persists beyond a few weeks, what can we expect from global oil prices and the resulting inflationary effects?

We believe that purchasing power is the only sane definition of money. Investors have fresh memories about how disruptive the sudden inflation that started in 2022 was. Consumers and financial markets would love to avoid another extended period of runaway costs.

As AI continues to creep into workplaces, what can we expect for global unemployment numbers and corporate earnings?

Will companies that employ fewer people report higher earnings? It’s likely, at least in the short term. But if job displacement becomes widespread, the knock-on effects are harder to predict. Companies are saving money, but if too many people lose their jobs, who’s buying what those companies sell? This question doesn’t have a clear answer yet.

We’ve been here before

For the long-term investor, the current uncertainty should not be cause for alarm. It should be a reminder that long-term success demands patience.

Every major technological shift in history, from electricity to the internet, brought disruption and uncertainty with it. Every geopolitical conflict introduced uncertainty that investors did not welcome.

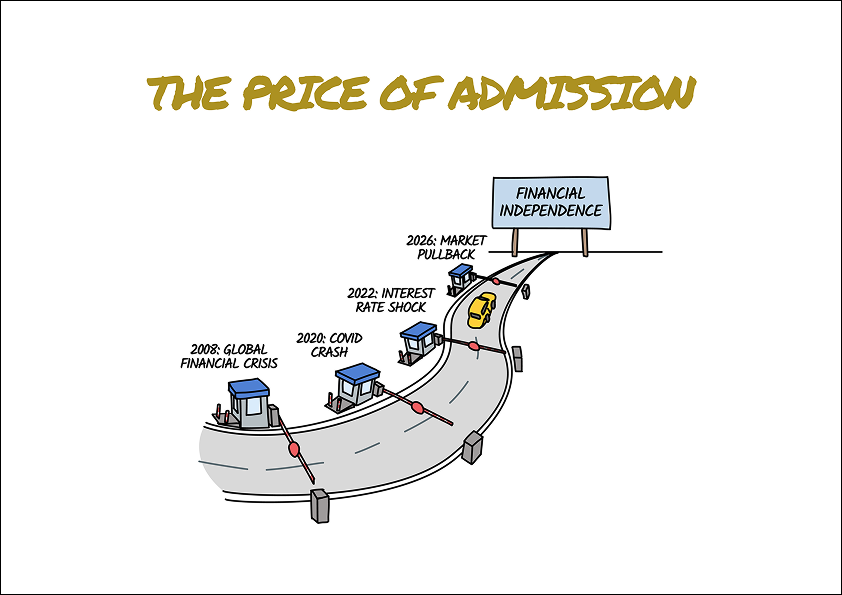

While unwanted, the resulting market decline has provided a test of patience that not all investors will pass. As we know, it’s these historically temporary declines that act as a price of admission that only some investors are willing to pay.

While we do not need to desire these periods, we should welcome them as a test of our patience and as a filter for which investors deserve the market’s long-term returns.

The temptation to act

The real danger of a market decline often lies in how we respond to it.

These moments often trigger the instinct to do something. To sell and to time the recovery feels like the responsible thing to do, and we can relate to this urge. However, the evidence has historically favoured those who stay invested in quality companies for the long term.

This advice may sound trite to the curious and problem-solving mind, but it’s the reality we need to face.

Investors who experienced the pain of the 2020 Covid era, the 2022 inflation era, and the 2025 Liberation Day tariffs are now being asked the age-old question:

“Is it different this time?”

Our answer is a firm “No”.

Every investor’s situation is different. If you’d like to discuss how current market conditions may affect your own financial plan, please reach out.

Written by:

Martin Tuttlebee, Managing Director

martin@metricwealth.com